|

|

|

|

|

|

|

Play the video. You will be shocked to see that even a United States Congresswoman, calling on behalf of her constituent seeking a loan modification, was stonewalled with bureaucratic red tape. "Dead end" after wasting hours on the phone!

I know 'how' to avoid these loan modification problems. So, if you have a sale date already scheduled, please don't waste anymore time and contact me to see if you are qualified for a loan modification. A loan mod can drastically lower your payment and eliminate all your arrears!

Depending on your exact situation, your lender should want to consider a loan modification. With a modification, it's possible to refinance the debt and/or extend the term of your original mortgage loan. This will make your new monthly payment affordable and allow you to build the missed payments into the new 30 year loan.

Loan modifications were very hard to come by in the past, but now, with all the new lending laws and government assistance, a modification can be as simple as correctly filling out the application. Although, hiring an attorney or mitigation expert is still a good idea.

You do not want to attempt a loan mod on your own unless you are absolutely sure it will get approved. You need to make sure it's done right the first time, or you could ruin your chances of making a second deal in the event you are turned down once. A mortgage modification makes it much easier for you make your monthly payments and catches you up on your arrears. |

|

|

|

|

|

|

|

|

|

|

|

First, it's important to know that there are many different modification programs and loan bailout plans. To qualify, you may need to meet certain circumstances. For example, there is a new government mortgage plan that will reduce your interest rate and re-amortize your loan, but you need to be current on the mortgage. If you have any late loan payments, you will not qualify.

But for other plans, you need to be late on the mortgage. Usually when you are 60 days late or more, your lender should be willing to talk to you directly about modifying your loan. But it's important to understand which type of loan or modification you should be applying for. I can help you with that.

Example of a Loan Modification

Here is a typical loan mod example:

Lets say your mortgage payoff is $200,000 and your current interest rate is an adjustable 9.35% and you are currently 5 payments behind on a $2300 mortgage payment.

For this example, lets assume you owe $200,000 and owe an additional $12,000 in arrears, for a total of $212,000.

Lets also say that based on your income, you can only afford a $1800 a month payment.

Based on these numbers, a loan modification we would try to negotiate would be a new 30 year fixed mortgage at 5.5%. This is a reasonable interest rate (we've seen rates negotiated as low as 2.5% or even 0% for a short time) and we would never stretch a loan out to longer than 30 years.

It's just not reasonable to pay on a loan for that long and the cost is much higher. In fact, we'd rather do a 15 or 20 year loan with a lower interest rate, to make it more affordable. This is better for your long term financial recovery.

With a modification, in this scenario, the new payment is nearly cut in half!

In this case, a modification would save about $600 a month after taxes and insurance are paid.

To qualify for a modification, first you'll need to prove there was a hardship or lender misconduct that caused the loan to become a problem. Then your income will be used to determine if you qualify for a modification. this is where it can get tricky.

If the forms are not completed correctly, or if your situation doesn't fit the lender's exact mold, then you may be immediately turned down. Once you are turned down, the lender will likely automatically turn down any future attempts to correct the problem as well.

This is where hiring a professional can be of great value. Knowing that it's going to be done correctly the first time is invaluable. Also having someone to negotiate when your situation doesn't fit the lender's exact "mold" is almost a necessity these days.

One mistake many people make when attempting a mod is to apply for it, then expect the foreclosure process to stop. This is why many people come to me just days before a sale asking for help. It's important to stay on top of things and to never trust your lender to automatically stop the sale for you.

Until your loan statement shows that you are current on your mortgage, or until you have something in writing that says your loan is current, you should always assume the worst!

|

|

|

|

|

|

|

|

|

|

|

|

No matter what others have told you, a loan to stop foreclosure is still possible. There are several lenders who will loan you money, regardless of your credit or your past mortgage loan history.

When you apply for a foreclosure loan, there are three major things the lender will look for; credit, income, and loan to value. If you are less than 2 months behind, then your credit is probably still acceptable. If you are more than 2 months behind, you may need more stable income and equity in your home to qualify for a foreclosure refinance.

While most mortgage loan companies have basic minimum guidelines to qualify for a foreclosure loan, the lenders we work with are more understanding of your situation. No one is turned down on the basis of credit, income, or equity, until each case is thoroughly reviewed.

Regardless of your credit history, or what others have told you, you may still qualify for a foreclosure mortgage loan. Even if you do not meet the requirements for this type of loan, many times exceptions are made to the rules, so it makes sense to find out if you can refinance your home out of foreclosure today.

Non-traditional foreclosure lenders and private foreclosure lenders are much more lenient with these guidelines and will sometimes lend you as much as 90% of your home's value, so never rule out a refinance to save your home from foreclosure. You may discover you could have refinanced your home only when it is too late. Do not let this happen to you.

|

|

|

|

|

|

|

|

|

|

|

|

Three different names for the same type of solution. Depending on your exact situation, your lender may be required to offer you a solution to repay your missed payments and avoid foreclosure with a Mortgage Forbearance Agreement.

These special repayment plans are called "Special Mortgage Forbearance Agreements" and you could request this type of payment plan. A special mortgage forbearance agreement is a written repayment agreement between a lender and a mortgagor that contains a plan to reinstate a foreclosure loan that is a minimum of three payments due and unpaid.

If you qualify for a Special Mortgage Forbearance agreement, you may be allowed to postpone monthly mortgage payments for a minimum of four months. While there is no limit on the maximum number of months for a mortgage forbearance agreement, at no time may the agreement allow the delinquency to exceed the equivalent of 12 monthly payments.

There are also special forms of repayment plans and forbearance agreements if you have a loan through Fannie Mae or Freddie Mac. These additional options are absolutely worth checking into!

Sometimes it is very easy to make these mortgage forbearance agreements with your lender; however, many lenders make this difficult for you to do on your own. I will help you work with your lender's loss mitigation department to determine if you qualify for the guidelines and give you the direction you need to work with your lender and set up a special mortgage forbearance agreement.

|

|

|

|

|

|

|

|

|

|

|

|

DO YOU FEEL YOU HAVE BEEN A VICTIM OF PREDATORY LENDING?

The only way to know for sure is to have your loan audited by a professional! Contact me to help you find out if you are one of the millions of predatory lending victims in the country.

Many homeowners who are experiencing difficulty staying current on their mortgage payments or worse...facing foreclosure today...are unaware that they were victimized! The only way to know for sure is to have your loan audited.

What defines predatory lending?

Steering & Coercing

Many homeowners were given sub-prime loans when they may have easily qualified for prime loans. Fannie Mae estimates that possibly up to 50% of the sub-prime refinanced loans could have been prime loans

Excessive Fees

A refinanced mortgage can be packed with excessive fees and/or unnecessary fees. A regular mortgage usually will have loan fees below 1% of the total loan amount. A predatory mortgage can have loan fees in excess of 5%

Insurance and Other Unnecessary Products

Predators often add insurance and other unnecessary products to the loan amount. The insurance they either insist on or intimidate the borrower into buying can include regular mortgage insurance, fire and hazard insurance, life insurance, disability insurance, homeowner's insurance, and health insurance.

Abusive and Abnormal Prepayment Penalties

Only about 2% of normal conventional mortgages have a prepayment penalty that might be difficult to meet. Up to 80% of sub-prime mortgage have an abusive prepayment penalty. Why? This is one more way the lenders made excessive money off of homeowners who were trapped into staying in an unaffordable loan because they could not afford to pay the cost of refinancing with the pre-payment on their loan.

Loan Flipping

When lenders find a homeowner whom they can talk or coerce into refinancing their mortgage, even though the homeowner gains nothing from the transaction once the fees and cost of the loan is taken into account. The process is called loan flipping.

Mandatory Arbitration

Another practice that falls within the definition of predatory lending happens when a lender hides words in the fine print that make it illegal for the homeowner to take legal action against the lender. The borrowers sign away their rights to sue the lender for any fraud, predatory actions or illegal actions. |

|

|

|

|

|

|

|

|

|

|

|

Among all the tools one should consider when facing foreclosure is the right of rescission. Rescission is the right to cancel the contract and unwind everything back to start. While a homeowner may have the right to rescind for a variety of reasons, I want to focus on one, the right of rescission under the Truth In Lending Act (TILA).

Every one who borrows money should be familiar with TILA. It is the law that require that prior to borrowing money, you be told the APR, the Finance Charge, the Amount Financed, the Total of Payments, the monthly payment amount, etc. It should show up as a box of information on the loan or in the case of a mortgage as a separate sheet. TILA requires that these disclosures be accurate within a certain tolerance, which if you are facing foreclosure is $35.

The right of rescission under TILA is a special tool that only applies under certain circumstances, so that it is often over looked. Rescission generally only applies to a loan which takes a security interest in the home of the borrower and was not used to purchase the home. For most this means a refinance or a home equity loan. You also have to be within 3 years of closing and still own the property.

|

|

|

|

|

|

|

|

|

|

|

|

Thus if you refi'd your home, which you still own, less than 3 years ago, and are now facing foreclosure read on:

***WHAT FOLLOWS IS A SIMPLIFIED DESCRIPTION OF THE ANALYSIS FOR POSSIBLE TILA RESCISSION FOR IMPROPER DISCLOSURE. IT IS INTENDED ONLY A QUICK GUIDE. IF YOU ARE FACING FORECLOSURE YOU SHOULD IMMEDIATELY SEEK HELP FROM A REALTOR WITH EXPERT KNOWLEDGE IN THIS AREA -- NOT SOMEONE WHO SENDS YOU A FLYER IN THE MAIL SAYING THEY CAN HELP YOU SAVE YOUR HOME. I AM NOT AN ATTORNEY OR C.P.A. IT IS HIGHLY ADVISABLE YOU SEEK ADDITIONAL CONSULTATION FROM A LICENSED PROFESSIONAL IN THESE MATTERS.

What you need to do is determine if your disclosures were accurate. If they are off by more than $35 you likely have the right to rescind.

Here's how to check. Get out your Truth In Lending Disclosure Statement and your Settlement Statement (also called a HUD-1).

On page 1 of the HUD-1 will be the amount of the new loan. For example purposes let's say the loan was $215,000.

Now look at the "Amount Financed" on the Truth In Lending Disclosure. in this example let's say the amount financed was $208,500. Why is the amount financed less than the amount of the loan? Because the "Amount Financed" is the amount of money that you actually got to use for refinancing. The $6,500 difference between the amount of the loan and the "Amount Financed" was actually prepaid finance charges.

Now here's where the work starts. Pull out page 2 of the HUD-1. Its the page with all the settlement charges, like brokers fees, taxes, closing costs, etc. Take a sheet of paper and make 3 columns. "Finance Charge", "Amount Financed" and "Questionable."

In the "Finance Charge" column place all the charges that are payable as a part of getting the loan. Think: "Would I have had to pay this charge if I had bought this house with cash?" If the answer is "NO" than it is likely a finance charge.

Anything that is listed as being paid to the lender or a mortgage broker should be in this column along with any prepaid interest. An exception to this is the Appraisal Fee, which is an "Amount Financed" so long as it is bona fide and reasonable.

Add this column up and it should equal the prepaid finance charges. The $6,500 in the example. If it is over by more than $35 dollars you may have the right to rescind. If its under recheck, you likely missed something. But that's not the end of things, you also need to look at the other charges.

All those other charges that you would normally have to pay if you were buying with cash, like closing fees, title search, title insurance, recording fees etc. are properly part of the amount financed as long as they are "bona fide and reasonable."

This means the amounts actually were paid to whoever and the amount was reasonable. For example if you were charged $1500 for title insurance on a $215,000 refinance when the market rate was $450 for such insurance, the extra $950 wasn't bona fide or reasonable. Or being charged a recording fee of $250 when actually only $50 was paid to the recorders office.

Sleuthing out whether these charges are bona fide and reasonable may take a bit of work, but one thing that can help is to go to the internet and look for "closing costs calculators YOUR STATE" or "closing fees calculators YOUR STATE."

A lot of closing companies as part of their marketing have these calculators on their websites. Get 3-4 such estimates and average them. If your charges aren't similar, there is a good chance your charges weren't bona fide or reasonable.

EXAMPLE: Lets say the example person actually paid $6536 in finance charges not $6500 as disclosed, what happens next? Well if you still own the home and it has been less than 3 years since the closing, then you send a notice of rescission.

Upon receipt of the notice the lender has to immediately cancel any security interest they have in the property. (This stops the foreclosure dead). Then within 20 days they must return all money or property given as earnest money, down payment or otherwise.

This mean the lender has to give you back all the money above the amount you actually got to use out of the loan. (This is the amount used to pay off your old loan, any credit cards paid off, and any cash you got at closing.) Back to the example of the $215,000 refinance: Let say they paid off a $190,000 loan, $5,000 in old credit cards and got $5,000 in cash at closing.

They got the benefit of $200,000. The remaining $15,000 now has to be returned, and all the principal and interest payments made on the loan. Let's say the monthly principal and interest payments are $1000/month and were paid for 24 months.

The lender has to give back $39,000, then the Examples would have to give it $200,000. But the Examples have $39,000 in cash so they actually only need $161,000. So now the Examples have a house worth say $230,000 and only need to get a loan for $161,000.

If the examples are in bankruptcy, the effect of rescission is even greater because the loan from the bank may be considered unsecured.

Remember this is a very simplified explanation, so see an attorney!

|

|

|

|

|

|

|

|

|

|

|

|

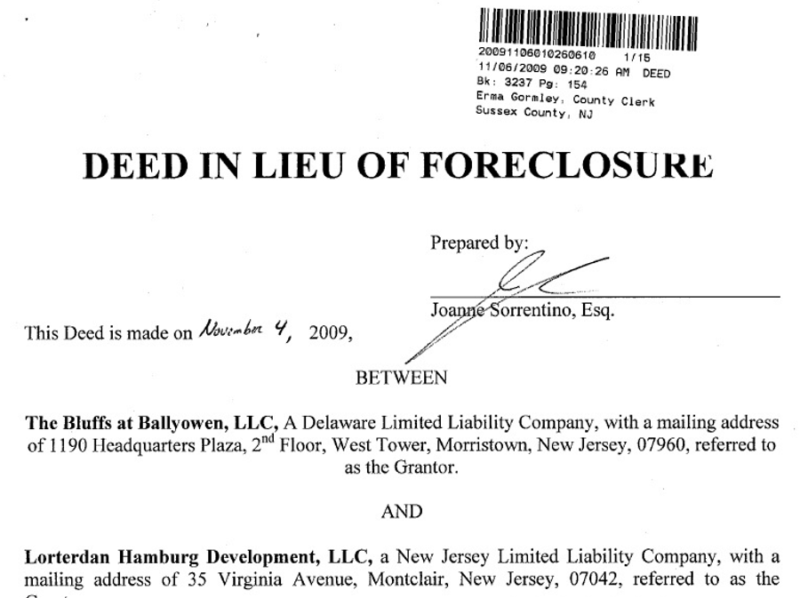

A Deed in lieu of foreclosure is a deed instrument in which a mortgagor (i.e. the borrower) conveys all interest in a real property to the mortgagee (i.e. the lender) to satisfy a loan that is in default and avoid foreclosure proceedings.

The deed in lieu of foreclosure offers several advantages to both the borrower and the lender. The principal advantage to the borrower is that it immediately releases him/her from most or all of the personal indebtedness associated with the defaulted loan.

The borrower also avoids the public notoriety of a foreclosure proceeding and may receive more generous terms than he/she would in a formal foreclosure. Another benefit to the borrower is that it hurts his/her credit less than a foreclosure does.

Advantages to a lender include a reduction in the time and cost of a repossession, lower risk of borrower revenge (metal theft and vandalism of the property before sheriff eviction), and additional advantages if the borrower subsequently files for bankruptcy.

In order to be considered a deed in lieu of foreclosure, the indebtedness must be secured by the real estate being transferred. Both sides must enter into the transaction voluntarily and in good faith. The settlement agreement must have total consideration that is at least equal to the fair market value of the property being conveyed.

Sometimes, the lender will not proceed with a deed in lieu of foreclosure if the outstanding indebtedness of the borrower exceeds the current fair value of the property. Other times, lenders will agree since they will end up with the property anyway and the foreclosure process is costly to the lender. |

|

|

|

|

|

|

|

|

|

|

|

When you file either a Chapter 13 or Chapter 7 bankruptcy, the court automatically issues an order (called the Order for Relief) that includes a wonderful thing known as the "automatic stay." The automatic stay directs your creditors to cease their collection activities immediately, no excuses.

If your home is scheduled for a foreclosure sale, the sale will be legally postponed while the bankruptcy is pending--typically for three to four months. However, there are two exceptions to this general rule:

Motion to lift the stay.

If the lender obtains the bankruptcy court's permission to proceed with the sale (by filing a "motion to lift the stay"), you may not get the full three to four months. But even then, the bankruptcy will typically postpone the sale by at least two months, or even more if the lender is slow in pursuing the motion to lift the automatic stay. |

|

|

|

|

|

|

|

|

|

|

|

Many people will do whatever they can to stay in their home for the indefinite future. If that describes you, and you're behind on your mortgage payments with no feasible way to get current, the only way to keep your home is to file a Chapter 13 bankruptcy.

How Chapter 13 works.

Chapter 13 bankruptcy lets you pay off the "arrearage" (late, unpaid payments) over the length of a repayment plan you propose--five years in some cases. But you'll need enough income to at least meet your current mortgage payment at the same time you're paying off the arrearage.

Assuming you make all the required payments up to the end of the repayment plan, you'll avoid foreclosure and keep your home.

2nd and 3rd mortgage payments. Chapter 13 may also help you eliminate the payments on your second or third mortgage.

That's because, if your first mortgage is secured by the entire value of your home (which is possible if the home has dropped in value), you may no longer have any equity with which to secure the later mortgages. That allows the Chapter 13 court to "strip off" the second and third mortgages and re-categorize them as unsecured debt --which, under Chapter 13, takes last priority and often does not have to be paid back at all.

|

|

|

|

|

|

|

|

|

|

|

|

It may be that you'll have to give up your home no matter what. In that case, filing for Chapter 7 bankruptcy will at least stall the sale and give you two or three more months to work things out with your lender. It will also help you save up some money during the process and cancel debt secured by your home.

Saving money. During a Chapter 7 bankruptcy, you can live in your home for free during at least some of the months while your bankruptcy is pending--and perhaps several more after your case is closed. You can then use that money to help secure new shelter.

Canceling debt. Chapter 7 bankruptcy will also cancel all the debt that is secured by your home, including the mortgage, as well as any second mortgages and home equity loans.

Canceling tax liability for certain property loans. Thanks to a new law, you no longer face tax liability for losses your mortgage or home-improvement lender incurs as a result of your default, whether you file for bankruptcy or not. This new law extends to the end of 2012.

However, the new tax law doesn't shield you from tax liability for losses the lender incurs after the foreclosure sale if:

- the loan is not a mortgage or was not used for home improvements (such as a home equity loan used to pay for a car or vacation), or

- the mortgage or home equity loan is secured by property other than your principal residence (for example, a vacation home or rental property).

This is where Chapter 7 bankruptcy helps. It will exempt you from tax liability on losses the lender incurs if you default on these other loans.

Chapter 7 Cannot Cancel the Foreclosure

With all this debt being cancelled, you may be wondering why the foreclosure on your home won't be cancelled too. The trouble is, when you bought your home you probably signed two documents (at least)--a promissory note to repay the mortgage loan, and a security agreement that could be recorded as a lien to enforce performance on the promissory note.

Chapter 7 bankruptcy gets rid of your personal liability under the promissory note, but it doesn't remove the lien. That's the way Chapter 7 works. It gets rid of debt but not liens--you'll still probably have to give up the house under the lien since that's what provided collateral for the loan.

Chapter 7 Bankruptcy May Not Be Right For You

Not everyone can or should use Chapter 7 bankruptcy. Here's why:

You could lose property you want to keep. Chapter 7 might cause you to lose property you don't want to give up.

As an example, if your wedding ring is particularly valuable, it may exceed the dollar amount of jewelry you're allowed to keep in a bankruptcy (under something called the "jewelry exemption"). In that case, the bankruptcy trustee could order you to turn the ring over to be sold for the benefit of your creditors.

You may not be eligible.

Even if Chapter 7 bankruptcy would work for you, you may not be eligible. Under the Bankruptcy Abuse Prevention and Consumer Protection Act of 2005, you are not eligible if your average gross income for the six-month period preceding the bankruptcy filing exceeds the state median income for the same size household. Nor are you eligible if your current income provides enough excess over your living expenses to fund a reasonable Chapter 13 repayment plan.

|

|

|

|

|

|

|

{kind=link}

{kind=link}